Doc's note: The economy and stock market are still booming, but now the financial "tide" is rolling out... The Federal Reserve is now raising rates and unwinding its massive stimulus program for the first time in nearly a decade. Credit is tightening, slowly but surely.

According to my good friend and Stansberry Research founder Porter Stansberry, there's one major consequence of this that nobody ever talks about.

Today, I'm sharing a recent issue of the Stansberry Digest, where Porter shares the details of this consequence, why he's concerned about the credit markets, and what these problems mean for the stock market.

What's happening now could lead you to the single best opportunity you'll ever have to make a literal fortune in the markets. And Porter is showing his Stansberry's Credit Opportunities subscribers the absolute best and safest way to take advantage of this opportunity.

***

On April 27, just over two months ago, I (Porter) wrote a Friday Digest warning you about a growing threat to our current bull market...

There are serious problems in the underlying fundamentals of our equity and credit markets. Rising interest rates are going to expose these problems, accelerating the inevitable end to the current credit cycle and this bull market in stocks.

In today's Digest, I want to update you on the indicators I told you to watch and discuss what the deterioration of these indicators means. Ideally, you'll be able to see for yourself that these problems are getting worse. What you can't do is rely on the mainstream media to warn you about a credit-default cycle. They will tell you the exact opposite of what you should know – all the way down.

So... with apologies to those this offends... remember that there's no such thing as teaching, only learning. Let me show you why I'm concerned about the credit markets and what these problems inevitably mean for the stock market. Please... don't hesitate to ask me follow-up questions or to pose alternative narratives. The more involved you become in these ideas, the better they will serve you.

And if you don't understand everything immediately, don't worry. These topics are complex. Just keep reading. Keep asking questions. Keep thinking about what's happening. Even if you totally disagree with me, you will still learn something, I'm sure.

As you might recall, the gist of the problem is simple...

For almost a decade, artificially low interest rates allowed individuals, businesses, and governments around the world to vastly expand the use of debt financing.

It hardly matters now, but this wasn't a mistake. The global interest-rate manipulation of 2009-2017 was required to save the global financial system as trillions of dollars lent against real estate and real estate derivatives were headed into default.

Losses of this magnitude had to be "socialized" – financed through a currency devaluation – or else almost every bank in the developed world would have failed, leading to massive losses for depositors. Depositors, as politicians would remind you, vote. And when their deposits disappear, they riot.

Alas, in a world dominated by democratic governments, banks won't fail but currencies sure will. (Sadly, that punishes savers and excuses debtors... producing an economic system that rewards perfidy. Ain't the government grand!)

But like I said, the why hardly matters anymore.

The question everyone should be focusing on today is how this unprecedented interest-rate manipulation/global devaluation will impact the markets going forward. What are the unintended consequences going to be?

There will be consequences, that's certain. There's no free lunch.

Here's one consequence nobody ever talks about...

There's been a massive decrease in the purchasing power of major paper currencies. Over the past 10 years, gold has risen about 50% from around $800 an ounce to more than $1,200. The value of gold didn't change a whit. It was the purchasing power of the dollar that fell.

The impact of this devaluation has been muted by rising productivity (thanks to technology), a massive increase in American oil production, and a generally weak global economy. But... there's no question that the collapse in real wages has led to a shift in politics around the world and a huge increase in the wealth gap between asset owners and labor.

What's another very important consequence? Let me explain it this way...

My family lost a beloved black Lab (Ringo) late last year. We got a new puppy (Hank) early this year. If you've ever fed a black Lab dog food, then you'll know exactly what happens when you tell businesses, consumers, and governments that they can borrow virtually as much money as they want for almost nothing. It's like an explosion in the dog bowl. Kibble goes everywhere. And it's hard to believe Hank doesn't choke himself to death trying to eat that fast. Well, the same has been true with credit issuance. It's been an explosion. Kibble has landed everywhere.

In America, federal debt more than doubled. Corporate debt soared to levels never seen before. U.S. non-financial corporations now hold a higher percentage of debt to GDP than ever before (over 45%!). We've seen five straight years of higher and higher levels of consumer debt (to over $13 trillion), far outpacing the total amount that led to the crisis in 2008.

And there's no sign these dogs are satisfied yet.

They're still gulping and slurping and throwing it everywhere. In fact, you'll never guess what's leading consumer debt higher now, at this stage in the cycle. You'll never, ever guess... mortgages... specifically, a new type of Fannie and Freddie mortgage product. It's called "The Conventional 97." It only requires a 3% down payment.

What's "conventional" about this kind of loan? Nothing, of course. No private lender would ever make a loan like this where the lender is taking all of the risk.

Who would make a loan like this? The government, of course. Our core economic policies are so incredibly harebrained that I can't make up a more ludicrous story. But this isn't a joke. It's actually happening. Mortgage balances are soaring. And, of course, home prices are too, far outstripping wage gains. You know what will happen next. Talk about "Groundhog Day."

The hard part about this kind of macroeconomic research/strategy is timing.

It's woefully difficult to know when a credit boom will become a credit bust. You should know that I thought the cycle was turning back in the fall of 2015. Interest rates couldn't get any lower... or so I thought. Then many sovereign rates went below zero! And the boom continued.

So... what's different this time? One critical thing.

The world's leading central bank – our Federal Reserve – is now raising interest rates. The most important interest rate in the world is the U.S. 10-year Treasury note. This is the most fundamental cost of credit, globally. This is the "benchmark" U.S. interest rate, and it is the price against which all other interest rates are measured.

In mid-2016, the yield of the U.S. 10-year hit an all-time low of 1.38%. It has since doubled, reaching more than 3%. (It now sits at about 2.8%.) A 10-year U.S. Treasury yield above 3% gives savers a "risk free" way to earn a reasonable return. For now, it beats inflation. This kind of safe, liquid "home base" for global capital hasn't existed in about a decade. And that's what's putting so much pressure on credit markets and foreign currencies around the world. A lot of capital would rather be safe than sorry.

So... you'll remember I told you to it's time to watch a few specific corporate credits.

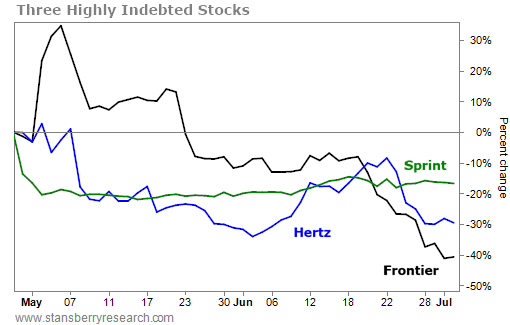

Three of the worst, highly indebted companies that can't afford their interest obligations include fixed line telecoms operator Frontier Communications (FTR), mobile telecom Sprint (S), and car rental company Hertz Global (HTZ). These stocks have all tanked. Since April 27, Frontier is down 41%. Hertz is down 30%. And Sprint is down 17%.

Frontier's stock chart looks like a major breakdown... like it's heading to zero, directly. Lot of money is at risk here: The company carries more than $17 billion in net debt. What's surprising is that the company's bonds (the Frontier 10.5% bond due in 2022) slipped below par ($100) in May last year and traded down to about $75 at the end of 2017. The bond market seemed to finally "get it." But since then, the bond is up more than 20% so far this year and is trading around the $90s today. That makes no sense. Are bond traders asleep at the wheel?

I've seen more and more of this lately.

Bond investors seem to be far too complacent today. We saw this last year with now-bankrupt toy retailer Toys "R" Us. Its October 2018 bond traded around par as late as last August before collapsing 80% to around $20 in a matter of two weeks. Bonds don't normally go from over par to less than $90 in a day or two. They don't normally go from above par to being in liquidation in less than a year. But that's happening more and more often. Why?

In the case of some corporate bonds, they're limited to institutional buyers and only a few trade each day. If you're going to use bond prices as a barometer of a company's health, you should make sure they're actively traded bonds. If not, you're probably buying a bond that simply doesn't have many people watching it closely, or the bond's owners don't have the liquidity to sell effectively.

Either way, the bond price you're thinking is reliable probably isn't. In general, bond market liquidity is way, way down since 10 years ago. That's changed the reliability of these prices.

I also told you to watch the big U.S. corporate high-yield bond funds.

The two major ones are the iShares iBoxx High Yield Corporate Bond Fund (HYG) and the SPDR Bloomberg Barclays High Yield Bond Fund (JNK). Both are down fractionally, so far.

As I said, the bond market, as a whole, has been slow to react to problems in this cycle, because it doesn't have nearly as much liquidity today. That's going to cause a big problem if investors all try to exit these funds at the same time (which, of course, they will).

Finally... the advanced part of this discussion...

If the idea of a "spread" between interest rates confuses the heck out of you, don't worry. It takes most people a long time to understand this concept.

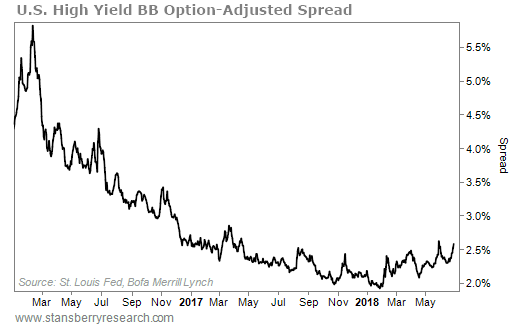

I'll try to make it as easy as I can for you to understand. Safe bonds, like U.S. Treasury securities, set a floor for interest rates. They're the safest bonds in the market, so they offer the least amount of yield for investors. You can measure how much risk is being priced into corporate bonds by comparing their yields with the government-bond yields. The difference is known as the "risk spread."

If I'm right and we're at the beginning of a big default cycle, we should see the risk spread growing as investors begin to demand more and more yield for the risk of holding corporate bonds instead of sovereign bonds.

Since early 2016, this measure of risk in the corporate bond market had been declining, from a spread of about 550 basis points (5.5%) to around 200 basis points (2%).

That is, holding a basket of high-yield corporate bonds was paying investors 2% more annually than holding U.S. Treasury securities with matching maturities.

To put it in even plainer terms... in exchange for holding corporate high-yield debt, instead of U.S. Treasury securities, investors were only demanding $20 a year more per $1,000 bond. At some point soon, the fact that investors were demanding so little premium to hold riskier bonds will be viewed as one of the most important signs of how far this credit bubble grew.

It is nuts to believe that a $20 annual premium is nearly enough compensation for the added risk of a high-yield bond compared with a U.S. Treasury.

The risk spread in the bond market has been growing since I wrote this warning in April. For the first time since January 2016, the spread seems to have broken an important technical barrier. It has "broken out" to a new high point on the chart. That could be an important signal of a trend change in corporate interest rates. The spread is currently greater than 250 basis points (2.5%). That's roughly a 25% increase off the lows.

I will start to get more interested in buying carefully selected high-yield corporate bonds (trading at a wide discount from par) when the risk spread goes over 500 basis points.

When that happens, you will be able to find bonds trading with 10% annual yields and total returns at maturity in excess of 15% annually. But... until then... I expect most high-yield bonds to be bad investments, on average. Likewise, you should strictly avoid owning any highly indebted stock, especially if it cannot currently afford its interest service.

I will continue to follow these trends and report on them as necessary in my newsletter, Stansberry's Credit Opportunities, which follows the corporate bond market closely and recommends distressed credits we believe won't default.

But you don't have to wait for the crisis to start profiting...

My Stansberry's Credit Opportunities subscribers have already seen impressive returns.

Since launching this publication in November 2015, my team and I have made 24 actionable recommendations of discounted or "penny" bonds. We've closed 15 of these positions so far for an average annualized gain of 33%. These returns trounced the 17% annualized returns you would have earned if you invested in the U.S. stock market instead. Yet we did it in the "boring" bond market... taking far less risk than buying stocks.

And all this before the biggest and best opportunities in the bond market have even arrived.

We just released a brand-new presentation where my team shares everything you need to know about these opportunities. Watch it – and learn how to get two free years of Stansberry's Credit Opportunities – right here.

Regards,

Porter Stansberry

July 5, 2018