In May, legendary singer Elvis Presley's Graceland estate was set to go up for auction...

A company called Naussany Investments & Private Lending claimed that Elvis' late daughter Lisa Marie Presley used Graceland's deed as collateral for a $3.8 million loan before she passed away.

In 2023, Naussany tried to settle the debt. It wanted to collect nearly $2.9 million from the Presley family trust.

Lisa Marie's daughter Riley Keough oversaw the trust. And when she pushed back, Naussany gave notice of an auction for Graceland.

Keough successfully sued to stop the sale. She claimed that someone had forged Lisa Marie's signatures in the loan documents.

And Naussany wasn't even a real company. A scammer appears to have created the entire entity.

As you would expect, not all property owners in the U.S. are as fortunate when it comes to detecting real estate scams. And that's why I (Marc Chaikin) believe one type of insurance in real estate is so critical...

For example, back in 1999, a man named William Gordon bought a 3.3-acre plot of undeveloped land in Arizona. He set it aside for building his retirement home.

Over the years, Gordon diligently paid the mortgage on the property. Then in March 2023, he suddenly got a letter from his title company congratulating him on the land sale.

Gordon's property had sold for $200,000 without his knowledge.

While he eventually won back his land, thousands of others weren't as lucky...

According to the FBI, 9,521 people suffered from real estate scams in 2023 alone. And they lost more than $145 million combined.

Meanwhile, a recent study from the American Land Title Association noted that seller impersonation is a growing problem in the real estate industry. According to the study, 28% of title-insurance companies saw at least one seller impersonation fraud attempt last year.

These fraudsters typically target non-occupied properties like Gordon's lot in Arizona and vacant homes. And as you can see in the chart below, the U.S. has millions of these kind of properties...

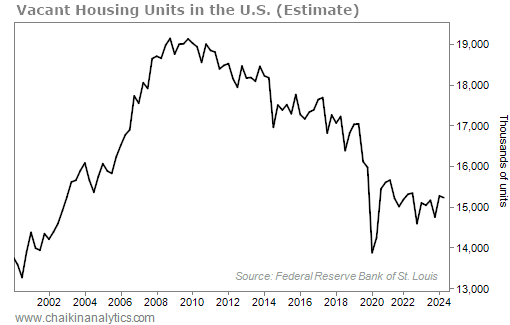

As of the second quarter of this year, the U.S. government classified more than 15 million housing units as vacant.

That figure isn't as high as it was during the subprime mortgage crisis and great financial crisis. But it's up about 10% from the pandemic lows.

Put simply, there's no shortage of seemingly easy targets for real estate fraud.

Now, the vast majority of privately owned properties in the U.S. have lender's title insurance.

That's because lenders require homeowners to take on this kind of insurance.

It protects the lender's financial interests as long as there's a mortgage on the property.

But many existing homes lack owner's title insurance. This protects the homeowner in the event of an undiscovered problem with a property's title.

More importantly, it can help provide a cash settlement to a new owner who unwittingly purchases a property from a fraudulent seller.

Without owner's title insurance, the person who bought Gordon's property in Arizona wouldn't have gotten back their $200,000.

Each year, about 1 out of every 5 homebuyers chooses not to purchase owner's title insurance.

That's a huge figure. And it exposes millions of people to potential fraud attempts – not to mention legitimate issues with a title that didn't come up during the homebuying process.

Now, you've probably noticed that the calls to lower the cost of homebuying are growing louder. Many folks feel like the industry stacks the homebuying process with unnecessary fees. And some have even called for the end of title insurance.

But as long as fraud exists... especially in a transaction as big as buying a home or property... title insurance will be part of the deal.

Yes, we all know that the housing market has been a mess. But millions of folks want to buy houses. Demand can't stay pent up forever. And when it unleashes, that means more title-insurances polices need to be written.

Put simply, this type of "boring" insurance isn't going away anytime soon. And the companies that provide it win when real estate changes hands.

Good investing,

Marc Chaikin

Editor's note: Marc predicted the 2022 bear market just days after the Federal Reserve's historic rate hike. Now, he is stepping forward to issue his next critical market warning. Right now, a signal is flashing that has gone off before every big crash of the past two decades. But he believes that the entire market won't suffer...