Doc's note: At the start of the pandemic, millions of office workers around the world were told to stay home. But as the pandemic wound down, lots of folks assumed office spaces that had been vacant would fill up with workers again.

Today, Rob Spivey, director of research at our corporate affiliate Altimetry, explains why this industry is still struggling to recover. And he explains what this means for investors everywhere...

We've been waiting for office real estate to recover...

And waiting...

And waiting...

And waiting.

Regular readers know the pandemic crushed this industry. The percentage of U.S. employees working from home tripled, rising from 6% in 2019 to 18% in 2021. And it still hasn't bounced back even as we move on from COVID-19.

These days, 13% of folks are still working from home. Freelance platform Upwork projects that percentage will rise to 22% by 2025... or 32.6 million Americans.

Office real estate has been clinging to life as companies trend toward hybrid schedules. But the problems are mounting... particularly in major metropolitan cities like New York and San Francisco, where "return to office" has been the most lackluster.

Put simply, the industry is in for even more trouble in the coming years...

In 2024 alone, companies have to repay or refinance $117 billion of commercial office mortgage debt...

That's bad news... because most commercial mortgages are interest-only until the final payment. Many real estate companies haven't owed much over the past several years. Their entire principal amount is due when the debt is due.

To pay off that principal, real estate companies will need to refinance. But interest rates have soared, and office buildings aren't bringing in as much cash flow as they used to.

Refinancing will be tough for many of the big U.S. office-building owners in today's high-rate environment. Moody's Analytics estimates that 224 of the 605 building owners with expiring mortgages will have trouble refinancing this year.

Without a clear full-time return-to-office trend, properties are stuck with more debt than they can handle.

And this year is only the start of the major problems for office real estate.

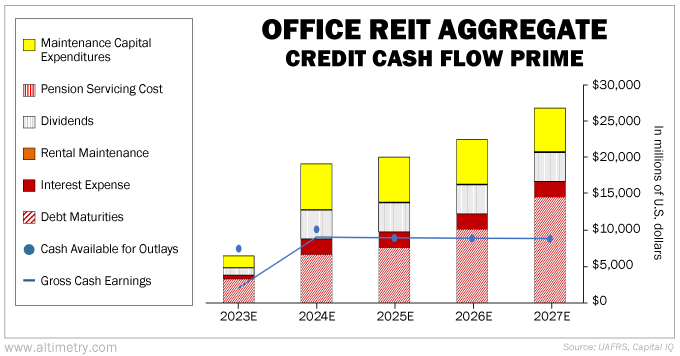

We can see this by looking at our aggregate Credit Cash Flow Prime ("CCFP") analysis for office real estate investment trusts ("REITs").

Our aggregate CCFP takes the Uniform cash flows and cash reserves for publicly traded U.S. office real estate companies... and compares them with their annual obligations.

In the following chart, the stacked bars represent office REITs' obligations each year through 2027. We compare these with cash flow (the blue line) and cash on hand at the beginning of each period (the blue dots).

Take a look...

As soon as this year, office REITs will struggle to cover all their obligations. They barely have enough to cover debt and interest. And as soon as 2025, they won't even have the cash to cover all their interest payments.

As the years progress, the debt maturities will keep mounting...

Offices will struggle to hold on to their tenants, and cash flows just won't be able to keep up.

Refinancing won't be an easy way out of this office-REIT debt hole. Even if they do refinance, their interest payments are going to go way up. It will only kick the can a few years down the road.

For investors, putting money in office REITs is even riskier than it often was before. Many could be facing bankruptcy in the months and years ahead.

And even those that manage to scrape by will likely disappoint the market. That will mean a big hit to their share prices.

This is yet another warning sign for the broader economy. While bankruptcies have started popping up, the worst is yet to come for risky areas like office real estate.

Regards,

Rob Spivey

Editor's note: Joel Litman, founder of Altimetry, is pointing to even more warning signs in the economy. According to Joel, a "Wall of Debt" could crash hundreds of public companies in the coming weeks. Click here to make sure you're prepared.