There's a long (and seemingly never-ending) list of reasons why investors should be concerned about the stock market right now.

There's the U.S. and China trade war... all-time-high stock valuations... rising interest rates... and one we've covered recently – mountains of corporate debt.

Lots of investors fear the repercussions of the growing amount of corporate debt, but should you?

That's what we're going to answer today...

First, it's important to understand how we got to where we are today... After the Great Recession of 2008 and 2009, the economy was so shaken up that no one was willing to borrow or spend anymore.

The economy needed a jump-start.

So the central banks like the Federal Reserve did two things to try and boost the economy. It cut interest rates down to all-time lows and bought Treasury bonds and mortgage-backed securities (MBS) to increase the money supply (known as quantitative easing).

It took a while, but eventually the economy recovered. And of course, all of this led to an increase in borrowing... Actually, a massive increase in borrowing.

Corporate debt skyrocketed nearly 40% since it peaked in late 2008. That means businesses have tacked on $2.5 trillion of debt in just under 10 years.

And in the past decade, it has made sense to take on debt. With interest rates so low, firms could buy back their own stock, increase dividend payments, make acquisitions, and invest in their operations.

Now to be fair, corporate debt is supposed to grow over time. The population increases over time and so does gross domestic product (GDP). Debt shooting up 40% sounds bad, but that's not the number you should be concerned with.

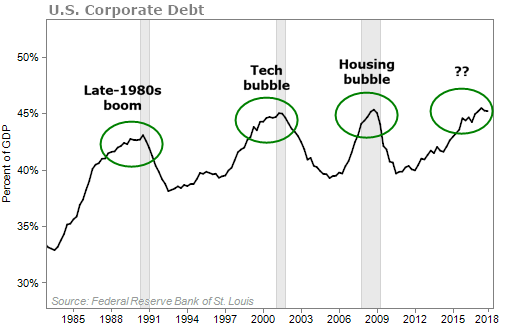

Instead, focus on corporate debt divided by GDP. It gives a clearer picture to how debt is growing in relation to the economy. It also points out when it may be time to panic...

As you can see in this chart, the last three recessions (in gray) occurred when the ratio of corporate debt to GDP hit all-time highs. The peak during the tech bubble occurred when debt was 45% of GDP and the peak during the housing bubble was 45.3%.

Just a few months ago, corporate debt made up 45.5% of GDP... a new all-time high. It's currently just below that at 45.2%.

If we have learned anything from history, this certainly doesn't look good. It's easy to make the case a recession is coming sooner rather than later.

However, don't hit the panic button just yet...

The stock market goes higher when companies post higher earnings. And that's what we've been seeing the past few quarters. Record-breaking profits have been the main driver propelling the S&P 500 Index to new highs.

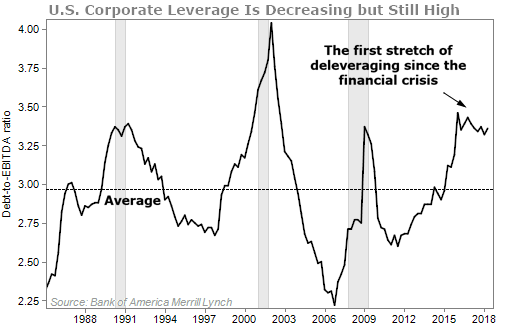

So when we talk about corporate debt, it makes sense to also compare it to earnings. If you analyze debt to earnings before interest, taxes, depreciation, and amortization (EBITDA), you'll notice that businesses are actually deleveraging...

According to data from Bank of America Merrill Lynch, the year-to-year growth of EBITDA generated by U.S. corporations has roughly matched or exceeded debt growth for six straight quarters. In the previous 21 quarters, the opposite was true.

This is encouraging. Earnings are growing and businesses aren't borrowing as much. Still, with a current debt-to-EBITDA ratio around 3.4, corporations are more leveraged than they were during the financial crisis, second only to when the ratio spiked to 4 during the tech boom of the early 2000s.

It's important to note that many companies haven't needed to issue new debt because of the savings they received from the recent tax-code change.

According to Dealogic, total bond issuance by investment-grade tech companies was only $21 billion from January 1 through August 23. That's down from $114 billion through the same period last year.

Bond issuance may very well pick up soon as companies burn through their tax savings.

In the end, debt may not be the cause of the next recession. But if corporations are still highly leveraged when a recession does hit, it's going to cause a lot of problems.

For now, I'm not losing any sleep over debt levels. The economy is too strong. With that said, I'm keeping a close eye on it... And if we do continue to see signs of deleveraging, investors should be very happy.

What We're Reading...

- Something different: Should you buy the new iPhone?

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig and the Health & Wealth Bulletin Research Team

September 19, 2018