Doc's note: Most folks like to follow the "smart money"... financial professionals who handle most of the trading in the stock and bond markets.

But in today's issue, co-editor of Stansberry's Credit Opportunities, Mike DiBiase, explains how you can actually make money when the professionals are wrong...

Every month, my colleague Bill McGilton and I scour through thousands of corporate bonds.

Normally, bonds are priced in line with the risk to the buyer... Safer bonds are more expensive and have lower returns, while riskier bonds are cheaper and offer higher returns.

Unlike the stock market, almost all the trading in the bond market is done by financial professionals at large institutions. They're the so-called "smart money."

They don't often make mistakes... But no one is perfect.

That's why we look for bonds that aren't priced correctly given their level of risk. We search for bonds that are far cheaper than they should be. In other words... we look for situations where the smart money is wrong.

Most people will tell you that trying to find these types of bonds – the "outliers," as we call them – is like camping out and hoping to spot Bigfoot. But we disagree...

Out of the thousands of bonds we sift through, we know at least a few will provide safe, outsized returns. It's our job to find them. Every once in a while, we find an outlier that's far cheaper than anything else in the market, given its risk.

Today, I'll give you a perfect example. You'll see how we get an edge on the investment pros... and exactly how lucrative these kinds of bonds can be.

It happened in November 2017...

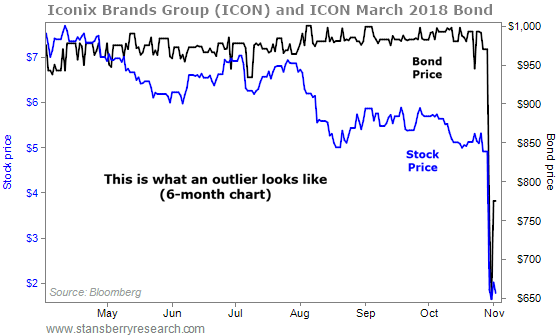

Brand-management company Iconix Brand (ICON) shocked investors with a troubling announcement. As a result, the price of its only outstanding bond crashed almost 50% in less than two full trading days.

We knew the market overreacted to the news...

And we didn't want the smart money to realize its mistake on this outlier before we published our regular issue of Stansberry's Credit Opportunities.

So we published a special update in early November 2017 for our subscribers. We recommended the company's 1.5% March 2018 convertible bond when it was trading around $770 per bond.

The bond's principal was due in a little more than four months. At its distressed price, subscribers could earn a massive 85% yield to maturity.

But how did we know the bond was safe? There were several reasons...

Iconix had a solid business with fat "cash profits." (Cash profits are simply the cash the company generates from its operations.) That's one of the key things we look for in a potential bond investment.

At the time, Iconix owned around 30 consumer brands across the globe – you've probably heard of many of them – including Candie's, Joe Boxer, London Fog, Mossimo, Ocean Pacific, Danskin, Ecko Unlimited, and Umbro.

But here's the part about Iconix we really loved... It was a highly capital-efficient business.

Iconix didn't own any factories. It didn't maintain any distribution networks. And it would never get stuck trying to unload stale inventory. Instead, it partnered with "licensees" who designed, made, and distributed the products.

These licensees would pay royalties to sell Iconix's brands. All Iconix had to do was market and protect its brands and trademarks.

That's why Iconix's cash-profit margins averaged more than 40%. This kind of cash margin is rare... It got us excited.

Iconix's long-term debt was around $820 million, and it was sitting on about $100 million in cash. The March 2018 bond we were eyeing had $236 million outstanding, and it was the company's earliest maturing debt. Iconix had just secured $300 million in new financing – enough to pay off the bond in full.

The smart money was confident the bond would be repaid – and it priced it accordingly. It traded near par value of $1,000 per bond and yielded around 4%. Everything was in order – just what you'd expect from another "boring" bond.

Then, in late October 2017, Iconix dropped a bombshell...

The company announced that Walmart would no longer sell Danskin – Iconix's 135-year-old iconic women's fitness brand – after January 2019. Iconix said it would miss out on around $16 million in royalty revenue.

Of course, that was only around 4% of Iconix's revenue...

But discount retailer Target (TGT) had already said it would drop Iconix's Mossimo clothing brand after January 2019. And Walmart (WMT) planned on dumping Ocean Pacific in 2019, too.

As a result, Iconix said it might not be able to comply with its debt covenants – financial restrictions imposed by its lenders, like keeping certain debt ratios under the bank's thresholds.

And because of this, the banks pulled the $300 million of new financing earmarked to pay off the bond. That put Iconix in a liquidity crunch... It had to come up with a new way to pay off the bond.

If it couldn't refinance, it would go bankrupt.

The stock and bond markets both reacted violently. As you can see in the following chart, Iconix's stock and March 2018 bond prices fell off a cliff...

The smart money lost confidence that Iconix would pay off the bond. The bond lost almost 50% of its value... falling from around $970 on October 27 to as low as $519 on October 31 before recovering slightly to around $770 per bond.

But we believed investors were severely overreacting to the news...

You see, the bank lenders left a lifeline for Iconix. They agreed to amend the loan and provide the financing if Iconix could meet a few further conditions...

First, the lenders cut the size of the credit line they were willing to extend from $300 million down to $225 million. That was still more than enough to pay off the bond in full.

More important, to secure the new financing, the banks said Iconix had to come up with $125 million in cash.

But we were betting that Iconix could get together the cash it needed...

Iconix had an impressive portfolio of brands and strong cash flows. We knew the company could secure the $125 million in any number of ways. That included issuing new debt, issuing new equity, or selling some of its brands.

And even if it couldn't do any of those, we knew that in a worst-case scenario, creditors would find a way to avoid bankruptcy...

Even if Iconix couldn't raise the cash, the banks said they were willing to accept a reduction of up to $100 million in the company's debt as a condition to provide the refinancing.

So at worst, bondholders could agree to accept $100 million less in principal. That meant, in the worst-case scenario, bondholders would collect $136 million of their principal ($236 million outstanding less the $100 million reduction). And we would collect at least $580 for every $1,000 of principal owed.

In other words... recovering 58% of the principal was the worst-case scenario. Even then, we'd get paid back most of our investment.

Of course, we would never have recommended this bond if we thought it wouldn't pay us in full. But we always want to understand our downside risk with any bond we recommend.

It's part of the careful work we do to find safe outliers... and to outsmart the smart money.

So what happened? How did this situation play out?

Just about three months after our special update, Iconix reached an agreement with its large institutional bondholders – investors who held $125 million of the bond we recommended. Those bondholders agreed to exchange their bonds for new bonds maturing five years later. That reduced the amount of debt that Iconix had to pay in March 2018 by $125 million.

For all other bondholders, including our Stansberry's Credit Opportunities subscribers, nothing changed. The exchange allowed Iconix to complete its refinancing and pay off the rest of its bondholders. They were paid on time and in full as expected in March 2018.

Subscribers who bought the bond when we recommended it in November 2017 earned a 31% gain in less than five months. That's an annualized gain of 85%.

People say that finding safe, deeply discounted distressed debt – like this Iconix bond – is impossible. But as I've shown you today, it's not impossible.

We let our subscribers know immediately when we find these opportunities so they can take advantage of them and earn huge, safe returns... right under the noses of the financial pros.

Good investing,

Mike DiBiase

Editor's note: You don't have to take it from us. A longtime subscriber recently shared how this technique helped him solve his financial problems. He made 660% in one case... 307% in another... and even 321% on his very first try. So we decided to give him the floor. And as part of the deal, we're offering a special Holiday bonus worth $1,200. Get all the details right here.