It's one of the first mega-deals of 2022...

Yesterday, Microsoft (MSFT) announced that it's buying video-game maker Activision Blizzard (ATVI) for a whopping $68.7 billion.

While Microsoft is mostly known for its Office products and its cloud-computing business, it has been involved in the video-game industry for years. Microsoft is the creator of Xbox – one of the most popular gaming platforms in the world.

With its acquisition of Activision Blizzard, Microsoft would become the world's third-biggest gaming company. Shares of Activision surged 25% on the news, while Microsoft shares were down slightly.

Activision is a company that we've liked and had an eye on for many years... It's a legendary gaming publisher with timeless titles like Call of Duty and World of Warcraft.

These powerhouse brands afford Activision a great luxury... All Activision has to do is come out with a new version of Call of Duty or World of Warcraft each year, and fans rush for their credit cards. This makes sales a little more predictable in the volatile gaming industry. Other video-game publishers have to strike gold with new titles every year to be successful.

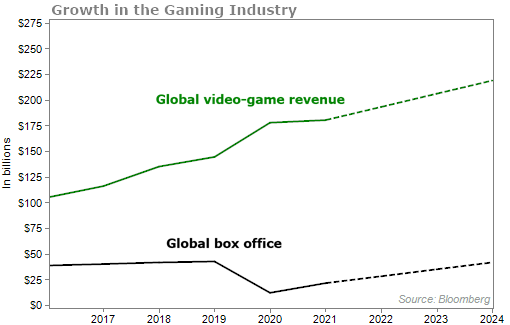

Gaming has been a rapidly growing industry over the years. According to Bloomberg, global video-game revenue was about $105 billion in 2016. It nearly doubled to $180 billion in 2020. And it's expected to cross the $200 billion tally by 2024.

The chart below shows you how gaming is now bigger than the movie industry...

Though Microsoft paid a steep price for Activision, we like the merger. These new games from Activision will help Microsoft expand its own offerings for the Xbox console. It will also help the company more directly compete with rival Sony (SONY), which makes the PlayStation console.

Now, let's see if Microsoft can afford this $68.7 billion mega-deal...

At the moment, Microsoft is sitting on $19.2 billion in cash and has $78.9 billion in total debt. That gives the company a net debt (debt minus cash) position of $59.7 billion.

To see if a company is overleveraged or not, we like to compare net debt to earnings before interest, taxes, depreciation, and amortization ("EBITDA"). We use EBITDA because it's often a shortcut to estimate the cash flow available to pay off debt.

The net-debt-to-EBITDA ratio shows how many years it would take for a company to pay back its debt. The higher the ratio, the less likely a company is to handle their debt burden... and the less likely it is to take on more debt to grow the business.

We typically like to see a company with a net-debt-to-EBITDA ratio of less than 4.

Over the past 12 months, Microsoft was able to generate $88.8 billion in EBITDA. So when you compare its net debt with EBITDA, it has a ratio of less than 1.

Microsoft has a fortress balance sheet. It can most definitely afford to take on more debt.

Moving forward, Microsoft will have two ways to grow sales... First, it can see terrific growth from its cloud-computing business, Azure, which has year-over-year growth of about 50% for each of the last nine quarters... Microsoft can also now grow from its new gaming business. Global video-game sales are projected to rise by more than 20% by 2024.

Over the years, my team and I have been bullish on Microsoft time and time again. We first recommended subscribers buy shares in November 2010 in Retirement Millionaire. Folks who took advantage of that recommendation are up 1,111% today.

We made another buy recommendation in December 2019, and shares have more than doubled since then. And just recently, we recommended a bullish options trade on Microsoft in my Advanced Options service.

Shares of Microsoft are down by about 10% this year... My advice is to take advantage of the dip and buy shares today if you don't already own the stock.

What We're Reading...

• Microsoft to gobble up Activision in $69 billion metaverse bet.

• Something different: Goldman shares drop 7% after earnings miss on surging expenses, equities trading slowdown.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig and the Health & Wealth Bulletin Research Team

January 19, 2022