A couple weeks ago, I asked subscribers to share their biggest concern about retirement. My inbox has been overflowing since...

Despite a recovering economy and a bull market, lots of you are worried.

I don't blame you. It takes years to build up a nest egg that you feel comfortable enough with to last your retirement. And it can take just a few weeks to watch it get cut in half.

We're in a market boom right now. That means a bust is sure to be right around the corner. Plenty of folks wrote in and asked how to handle the coming Melt Down.

But surprisingly, that wasn't the No. 1 concern for retirement though...

It turns out that folks are more worried about the looming threat of inflation.

Inflation reduces purchasing power. For retirees, your health care becomes more expensive, as well as your housing costs and even your groceries. Simply put, a dollar won't buy as much as it used to before a surge in inflation. And that means you run the risk of outliving your money.

It's scary to think of. No one wants to be forced back to work when they should be on a beach sipping Mai Tai's.

As an example of how inflation can crush a retiree, take a couple with $1 million saved for retirement. They expect to spend $50,000 a year on expenses and trips to see their children and grandchildren. Let's assume they earn 3% on their money in safe bonds.

Now, if there is 3% annual inflation, that $1 million would last for 20 years. But if inflation rose to, say, 12% a year... that $1 million would run out in 11 years and nine months. In this scenario, returning back to work becomes a real possibility.

Now, 12% inflation is unlikely. But you get the point. Even an inflation rate of 4% or 5% can reduce the amount of time you can live on your nest egg.

And it turns out that Stansberry Research subscribers aren't the only one's worried about inflation...

Given the trillions in spending that our government has been pumping out lately, inflation is the latest buzzword. Flooding the economy with all that cash will definitely lead to more dollars chasing the same goods... and that means rising prices.

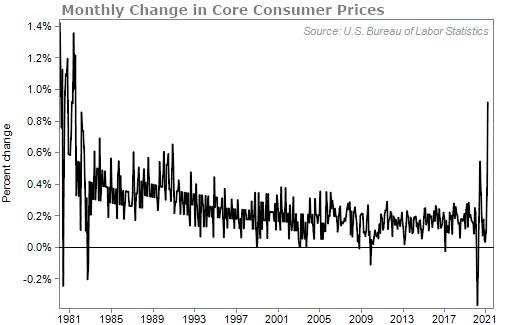

Last month, investors got a wake-up call when the core CPI, or Consumer Price Index, rose 0.9% month over month – an annualized rate of 11%. The core CPI is a key measure of inflation, and it's what economists tend to focus on because it strips out volatile food and energy prices.

As you can see, it was the biggest monthly change in years...

Raising interest rates is one way to cool inflation. When rates are higher, consumers tend to save more and spend less because they can earn higher returns on their savings.

But the Federal Reserve has been adamant that it will not raise interest rates any time soon. And that's why a lot of folks think inflation can run pretty high over the next few years.

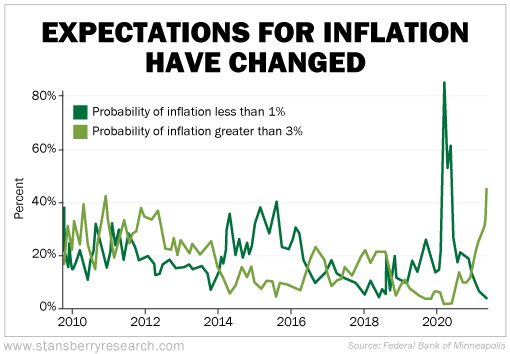

Options traders are betting on it. The chart below shows the option-implied probability of inflation over the next five years.

In March of last year, folks weren't worried about inflation. They thought it would be under 1%. But today, option prices are implying there's a 44% chance of inflation being above 3% over the next five years. It's the highest reading over the past decade.

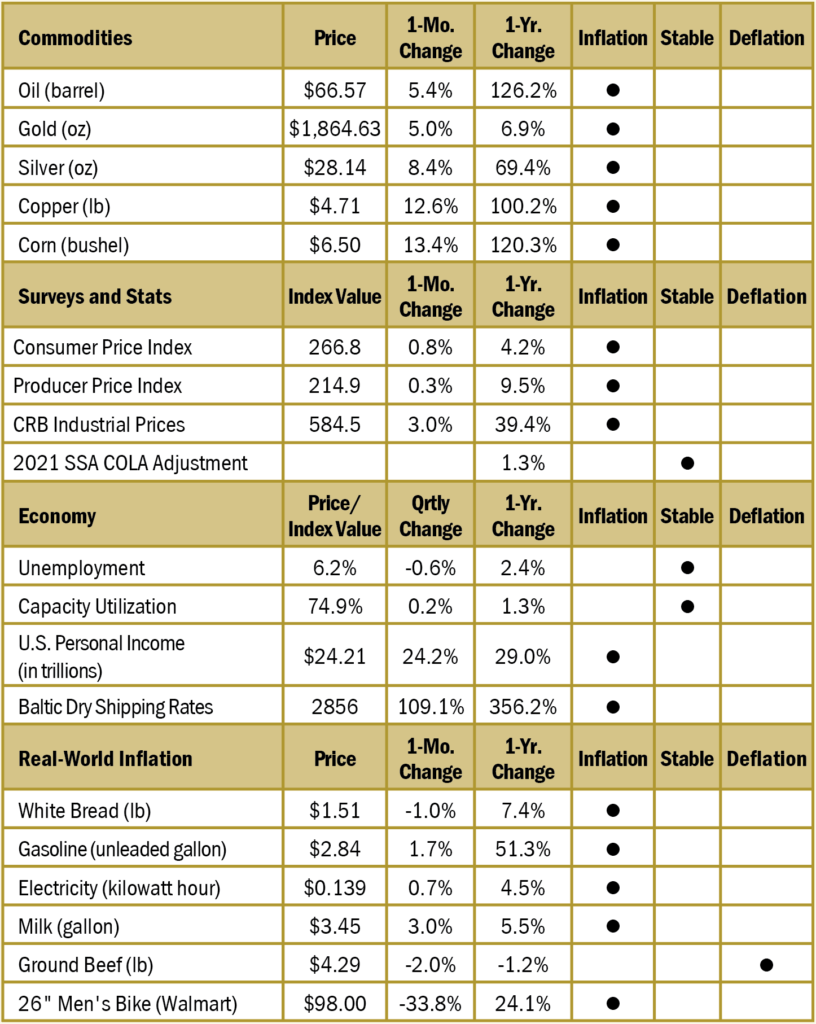

We track inflation each month in my income-focused newsletter Income Intelligence. Instead of just focusing on the core CPI, for example, we look at a number of inflation indicators – from commodities prices to real-world prices like the price of a bike at Walmart.

We're showing that 15 of our indicators are flashing inflation, and that's one of the highest readings we've ever had.

Now, this month's readings clearly reflect large "base effects." For instance, in May of last year, oil sat at $29, clearly due to pandemic-related shutdowns. That makes the 51% increase in gasoline prices, the 126% jump in oil, and the wild 356% rise in shipping rates "transitory."

However, it's obvious there's also still an underlying rise in inflation.

So whether you like it or not, inflation is going to be an issue. Retirees should be concerned by it.

That's why my team and I have been hard at work putting together an event addressing everything "retirement"... from the downfall of the 60/40 portfolio to ways to help combat inflation.

You'll hear more from me over the next few weeks about this event and how you can sign up. It'll be 100% free and again, I think it's a must-attend for anyone in or getting near retirement.

In the meantime, if you haven't already, I encourage you to check out a presentation by Wall Street veteran Marc Chaikin. Our firm has partnered with Chaikin to help share his decades of experience in financial markets with the masses.

In the presentation, Chaikin talks about his "Power Gauge" – a tool that truly levels the playing field with Wall Street. You can click here to learn more.

What We're Reading...

- Something different: Meditation helps Phil Mickelson win another PGA Championship.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig and the Health & Wealth Bulletin Research Team

May 26, 2021