Retirement accounts across the country are suffering...

According to a new survey by personal finance company MagnifyMoney, many Americans have either stopped contributing to their retirement accounts or have decreased their contributions because of the coronavirus crisis. Even worse, some Americans are pulling money out of their retirement accounts to pay for essentials.

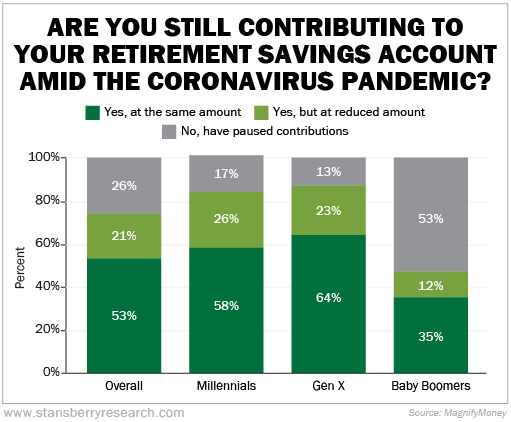

The survey went out to people of all ages that had a retirement savings account. When asked the question "Are you still contributing to your retirement savings account amid the coronavirus pandemic?" just under half of all respondents said they stopped their contributions or at least lowered them.

And as you can see, the Baby Boomer generation (ages 55 to 74) has been impacted the most...

This is troubling because folks in their 50s and 60s are the ones who need to keep their contributions steady. No one wants to get to the finish line only to be a few thousand dollars short.

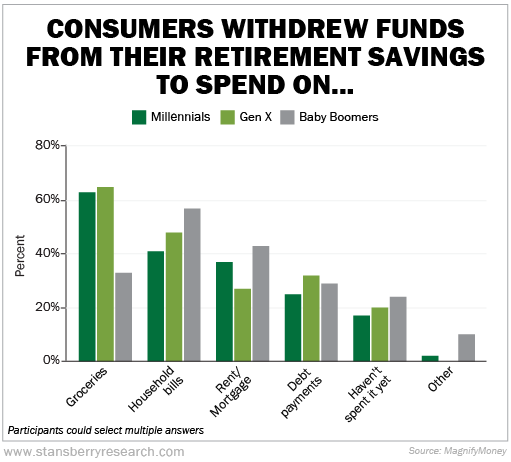

But the scariest result of the survey is that half of Americans have either pulled money from their retirement accounts in the last two months, or they plan to shortly.

Some of this can be explained by folks taking advantage of new legislation allowing penalty-free withdrawals... But the majority of people pulling money from retirement accounts are doing it to cover expenses. That means they've been short when it comes time to pay for groceries, rent, or utilities.

The majority of Baby Boomers said they needed the money to go towards household bills. The majority of millennials and Gen Xers needed the funds for groceries...

It makes sense that folks are searching for ways to come up with cash. More than 36 million jobless claims have been filed in the last two months. And the unemployment rate is now more than 14% – a level which hasn't been seen for decades.

It's just unfortunate that many have had to turn to their nest eggs to cover necessary expenses.

I've talked a lot about the economy, the stock market, and the coronavirus over the past few weeks, but today I want to cover some basics of personal finance.

Many people in the U.S. have adopted the attitude of just surviving this crisis. But I don't want Health & Wealth Bulletin readers to forget about an important goal... And that is being able to retire when you want to and being able to live comfortably in retirement.

Today, let's go over three important topics... Your ideal savings rate, housing and other debt levels, and how much you need in case of an emergency.

1. How much should you save per year?

As I've talked about many times, if you want to be successful in life, you need to save. There's no other way around it. You can't rely on the government or anyone else to take care of you when you enter your golden years

If you haven't saved enough money, it will be hard to live the retirement lifestyle you are hoping for.

At a minimum, you should save 10% of your gross salary. This includes employee and employer contributions.

Let's say you have an annual salary of $80,000 and you're paid bi-weekly. If you contribute 5% of that to your 401(k) plan and your employer matches your contribution up to 3%, you'll end up saving $6,400 each year. You also set aside $500 every year in your savings account, bringing your total savings to $6,900. Divide that by your gross salary of $80,000, and your savings rate is 8.6%.

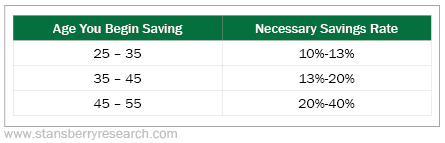

In the long term, you'll need to start saving more. Of course, how much you need to save depends on your age...

Every situation is different, but in general, you should follow these guidelines.

If you have children, grandchildren, or nieces and nephews starting out in their careers, be sure to stress the importance of saving. The earlier the better.

And even if you haven't been saving since age 25, it's never too late to start. Make saving money a priority. Make it a habit. Go without a $100 meal once a month and sock that money away for retirement instead.

It's simple, but saving as much as you can is probably the wisest lesson I could give anyone...

2. How much debt should you have?

For most of us, a house is the most expensive purchase we'll ever make. You want a house that you can live comfortably in, but you also don't want to get in a hole paying a mortgage or rent you can't afford.

As a general rule, your housing costs should be less than 28% of your gross pay.

Housing costs include principal, intertest, taxes, and home insurance. So if your total housing costs are $2,000 each month, you'll need a monthly income of at least $7,142 per month, or about $85,000 per year.

If you calculate your housing costs and you're over 28%, you're paying too much for your housing. It might be time to downsize.

And as you approach your retirement age, your housing costs should decrease and only make up about 5% of gross pay.

Also, if you throw in other debt such as car loans, student loans, or credit-card payments, your total debt shouldn't exceed 36% of your gross salary.

Here's the formula...

(Housing Costs + Other Debt Payments) / Gross Pay ≤ 36%

Interest rates are practically zero, so borrowing is cheap today. Keep this formula in mind when you're thinking about taking on more debt.

And ideally, your total debt should be about 10% or less of gross pay for those folks near retirement age.

3. How much of a rainy-day fund should you have?

We talked about the importance of an emergency fund or a rainy-day fund a few weeks ago. You should always have about three to six months' worth of expenses in cash.

In case you lose your job, you'll need such a buffer for unexpected costs such as medical bills or your car suddenly breaking down. (Or if a virus spreads across the U.S., causing much of the economy to shut down.)

Be sure that when you calculate your monthly expenses, you include items such as groceries, school expenses if you have children, clothing, and insurance. Don't include discretionary expense like vacations or premium cable channels. In times of emergency, you can go without those.

How much of an emergency fund you need also depends on your situation. If you are the sole provider in your family, you should have an emergency fund closer to six months' worth of expenses. If you and your spouse are both employed and both bring in roughly the same income, you could probably get away with three months' worth of expenses.

But no matter what, always have an emergency fund at a minimum of of three times your monthly expenses. It should never be below that.

If in times of crisis you need to dip into your emergency fund, make it a priority to replenish it shortly after.

Coronavirus and unemployment headlines are dominating the news right now and that's what most folks are talking about... But don't lose sight of your financial goals.

No matter what age you are, SAVE... Keep your debt levels under control... And always be prepared for an emergency.

Also, did I mention the importance of saving?

What We're Reading...

- Three in 10 Americans withdrew money from their retirement savings amid the coronavirus pandemic.

- Something different: These folks are working from their cars, and loving it.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig and the Health & Wealth Bulletin Research Team

May 20, 2020