Warren Buffett is perhaps the very best investor in the world... But he couldn't have done it without his right-hand man.

Early on in Buffett's career, he was a disciple of Benjamin Graham – considered the father of value investing.

When Buffett picked up a copy of his book The Intelligent Investor in 1949, his life changed forever. Truman Wood, Buffett's roommate in college, said that "it was almost like he found a god."

Buffett became obsessed with finding a "margin of safety" with his investments. This simply means that you purchase a security when its market price is significantly below its intrinsic value.

In the 1950s and 1960s, Buffett made a killing with his deep-value investing strategy. As Buffett said in a 1993 talk at Columbia University...

I found Western Insurance in Fort Scott, Kansas. The price range in Moody's financial manual... was $12 to $20. Earnings were $16 a share. I ran an ad in the Fort Scott paper to buy that stock.

I found the Union Street Railway, in New Bedford, a bus company. At that time it was selling at about $45 and, as I remember, had $120 a share in cash and no liabilities.

Decades ago, value investing was still in its infancy. Of course, information was not as widely available back then as it is today. Buffett was able to find these companies trading for huge discounts because, more than other investors, he put in the time to look for them... and was able to understand the real value of a company.

Thanks to his value-based strategy, Buffett made a lot of money in his early partnerships.

Then Buffett met Charlie Munger in 1959. Like when he picked up a copy of The Intelligent Investor, Buffett's life changed once again.

He would soon lose his devotion to deep-value investing. As Buffett wrote in 2012's annual letter for his Berkshire Hathaway (BRK-B) holding company...

More than 50 years ago, Charlie told me that it was far better to buy a wonderful business at a fair price than to buy a fair business at a wonderful price. Despite the compelling logic of his position, I have sometimes reverted to my old habit of bargain-hunting, with results ranging from tolerable to terrible. Fortunately, my mistakes have usually occurred when I made smaller purchases. Our large acquisitions have generally worked out well and, in a few cases, more than well.

Look at Berkshire today. It hardly focuses on traditional, unwanted value stocks.

Berkshire's top holding is Apple (AAPL), at 44% of the portfolio. The conglomerate first began buying Apple in the first quarter of 2016.

At the time, Apple was trading for 2.7 times sales. That's not egregiously overpriced for such a high-quality business. But it wasn't deep value. It was trading for more than the S&P 500 Index at the time, at 1.8 times sales.

Today, Apple trades for 27 times earnings and 6.8 times sales. And Berkshire keeps adding to its position.

Berkshire has also famously made a killing with its Coca-Cola (KO) investment. Today, Buffett and Munger own 9.2% of the company. And they haven't sold... even though valuations have swelled to 25 times earnings and 6.3 times sales.

Buffett now lives by the mantra of buying wonderful businesses at fair prices. And it's a good thing Buffett listened to Munger all those years ago.

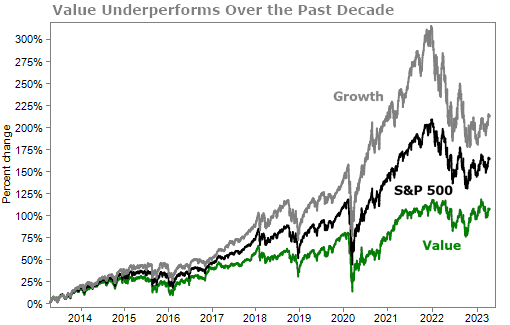

The past decade has been rough for value investors...

One trouble is that financial data is now so widely available. Everyone is operating on the same playing field nowadays. You could also blame the algorithms that automatically buy stocks the second they dip into value territory. Or you could blame the market's obsession with growth in recent years.

Here at Health & Wealth Bulletin, we agree with Munger's (and now Buffett's) outlook. Price matters, but quality matters more.

Do yourself a favor and don't pigeonhole yourself to be just a value investor or just a growth investor. Instead, focus on quality. Buy capital compounders and hold for the long term.

That's the key to making market-beating returns over time.

What We're Reading...

- Something different: Chegg shares drop more than 40% after the company says ChatGPT is killing its business.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig and the Health & Wealth Bulletin Research Team

May 3, 2023