It was a gutsy move. A confident, brash, and prescient market call.

Naturally, Kelly's friends warned her not to do it.

"Kelly, you're nuts," they said. "We wouldn't touch that stock with a 10-foot pole."

But Kelly knew she was right. She rolled her eyes at the warnings and bought shares that the rest of the market was selling off hard.

She made a killing...

Kelly defied the market because she knew something it didn't – a common-sense secret that I (Bryan Beach) will share with you today.

All names and certain details in this story are changed to protect identities. But everything I'm going to tell you about Kelly's unprecedented market call is true. I watched it unfold. And it changed the way I think about the markets...

At the time, I was a director in the accounting department of a well-run company that we'll call "Impact Synergies." Kelly had previously been one of my bosses at Impact. Earlier that year, Impact merged with one of its chief rivals, a company we'll call "Acquirer." As a result, Kelly took a huge buyout, leaving the company and riding off into the sunset.

Almost immediately after the merger, Acquirer revealed it would have to restate seven years of previously filed financial statements. In short, Acquirer had been reporting its revenues incorrectly.

It was the beginning of a huge sell-off in shares...

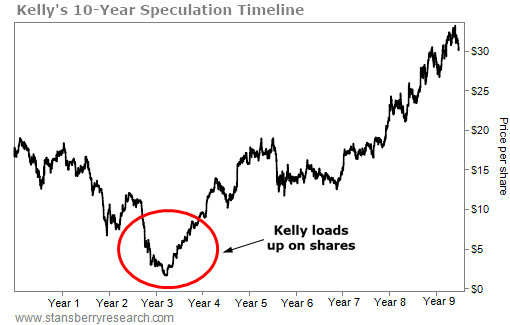

Impact began missing filings, held up by the restatement. Investors were soon completely in the dark about our current business operations. Our share price fell from $20... to $15... to $5, ultimately settling to less than $2 per share.

As Impact endured this death spiral, we started to hear rumors. Kelly – who had been gone about a year – was loading up on as many shares as she could.

It was a risky move...

The U.S. Securities and Exchange Commission (SEC) closely monitors unusual trading in companies during restatements. Insiders are not allowed to buy shares during that time. Of course, Kelly wasn't an insider anymore. But even a former insider loading up on shares could raise questions. When asked how her purchases might look, she simply stated the obvious:

I haven't been an insider in more than a year. Besides, I don't need inside information to know Impact isn't a $2 stock. All I need is common sense.

As the months ticked by, our company just kept rolling along, doing what it always did... selling software and services with fat gross margins of nearly 70% and collecting checks.

The business was fine. Our bank account was fine.

I knew that... But how could outside investors know it? And how did Kelly know?

It comes down to cash flow...

Free cash flow ("FCF") is the cash left over after a company pays all its bills and invests in all necessary infrastructure and maintenance. It's the most important metric in investing because it's almost impossible to manipulate. Earnings can sometimes be "managed," if nefarious management teams are so inclined... But you can't fake cash coming into a company's bank account.

That's why FCF is more important than any balance-sheet ratio you can devise... and a lot more important than the earnings numbers the media and Wall Street obsess over, or which period you recognize revenue in. Companies that generate lots of cash are solid businesses. And the market will always pay premiums for them – eventually.

Like me, Kelly had lived through accounting restatements before... And while the size and reasons for them can be vastly different from one company to the next, she knew this one wouldn't change anything about Impact's business.

More important, Kelly knew that you don't necessarily need mountains of data to assess cash flows. She didn't need a fancy spreadsheet. And she certainly didn't need inside information.

Her logic was simple: Cash flows don't lie.

Prior to the merger, Impact and Acquirer had both generated gobs of cash. Both companies had innovative products, loyal customer bases spanning the entire globe, and talented programmers. And all of that was public information.

Kelly knew that these companies weren't going to stop generating cash just because some accountants had to spend a couple years counting beans in silence. So when the stock dipped below $5, then $3, then $2... she pounced.

Sure enough, when we accountants emerged from our restatement cocoon and caught up on our SEC filings, the market realized what Kelly knew all along – our company was doing fine. I have no idea when Kelly sold... but Impact shares climbed more than 1,000% in about five years.

Every situation is unique. But now and then, an opportunity comes along to defy the market with a common-sense call – and make multiple times your money.

Not all restatements end up this way. In fact, we wouldn't touch most accounting restatements with a 10-foot pole. I'm a CPA with extensive experience working through these types of situations and have built up a certain level of comfort when evaluating these ideas. They're not for everyone.

The lesson here is not to pile into every delisted company going through a restatement. This is a lesson about the power of cash flows as a business metric. Restatement or not, we often see investors fleeing a solid, cash-generating business for short-sighted reasons. Next time you see that happening, remember Kelly.

Her secret was simple... Cash flows don't lie.

Good investing,

Bryan Beach

Editor's note: According to Bryan, the market is full of "blind spots"... huge moneymaking opportunities that most investors miss because of overall market sentiment or news skewing their perception and diverting their attention away from a sector or company. And right now, there's a rare opportunity today to double or even triple their money in as little as 18 months in these blind spots. Click here to learn more.