Doc's note: Valuation matters. Buying businesses at cheap prices will always beat buying them when they're expensive. The same holds true with stocks, but how do you know when stocks are cheap?

Today, my colleague and True Wealth Systems editor Dr. Steve Sjuggerud shares his secret on valuing stocks.

And if you want to know some of the best stocks to buy right now, check out True Wealth Systems. Just last week, Steve released a portfolio of nine investments to profit from his "Melt Up" thesis.

Quick! What's the most classic measure of stock market value?

If you said "the P/E ratio," then congratulations… You are right.

Next question! Are stocks cheap or expensive today?

Yes, it's a trick question…

If you've been reading my work recently, then you probably know my answer already. Stocks are actually cheap according to the main long-term measure of value.

The problem is, if you say this to the people in your life, most of them won't believe you…

Everyone knows that stocks have gone up for almost 10 years now – without a losing year. So it would be crazy for stocks to be cheap today, right?

Today, I'll tell you a secret nobody wants to hear: It's not crazy at all…

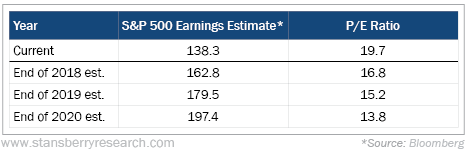

Let me share one number with you: 13.8.

That's the price-to-earnings (P/E) ratio of the U.S. stock market, based on analyst estimates of stock market earnings over the next two years. This is also known as the two-year forward P/E ratio.

This, my friend, is a low number… It's lower than its average value, going back 22 years.

Let me repeat that… The two-year forward P/E ratio today is below its average value going back to 1996.

How could the two-year forward P/E ratio be low after 10 years of good times in stocks?

The answer is simple: Earnings growth.

Some numbers from Bloomberg tell the story…

U.S. corporate earnings are growing at an astounding pace. And the consensus of analysts surveyed by Bloomberg is that earnings growth will continue. Take a look…

Specifically, analysts expect corporate earnings to grow from 138 this year to a whopping 197 by the end of 2020, two years from now. So when we look at the P/E ratio, if we leave the "P" the same, and we plug in those future numbers for the "E" – we end up with a radical result: Stocks are below their average value since 1996.

Will these analysts be right about future earnings? We can't know for certain. But short of a crystal ball, analyst projections give us a pretty good idea to work with.

My point today is simple:

- Don't let 10 years of gains in stock prices cloud the truth.

- Thanks to crazy earnings growth, the two-year forward P/E ratio of stocks is below its average value going back to 1996.

- Today's valuation is not "standing in the way" of even higher stock prices.

I am certain plenty of folks will want to argue with me…

They have made up their minds that stock prices have to fall… So they only look for facts they can use to confirm their belief.

But what if we just look at the basic facts, by themselves?

The P/E ratio is the all-time classic measure of value… And the two-year forward P/E ratio is trading just below its average value over the past 22 years.

Those are the facts.

And that's why I will keep on shouting them from the rooftops…

Most people believe that – after 10 years of higher stock prices – stocks can't possibly go higher. The secret is, they can…

And as we enter the final stages of the Melt Up, the time to profit is now.

Good investing,

Steve